Weekly Coal Index Report

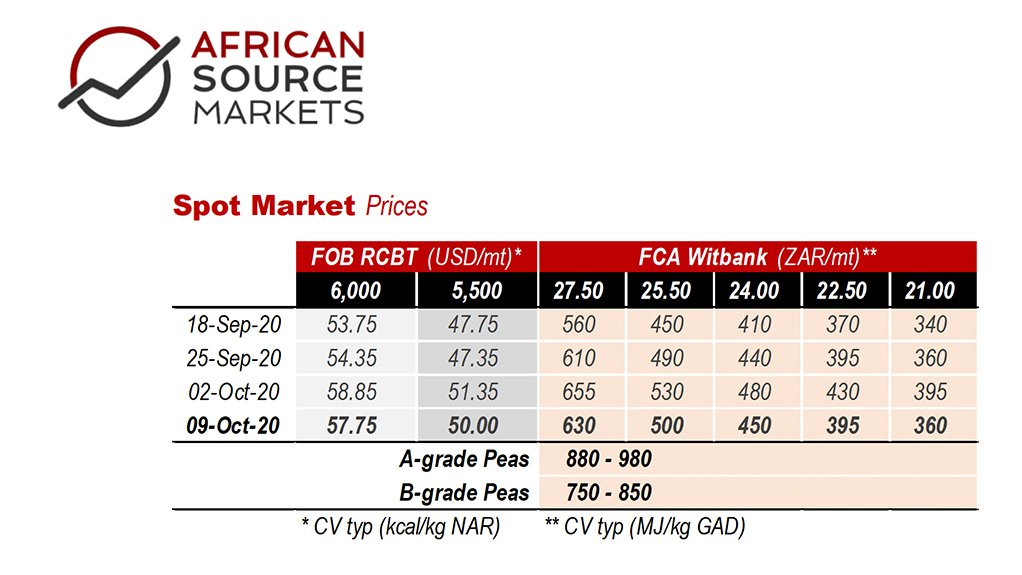

After October’s stronger rollover, last week saw subdued pricing for Newcastle, as concerns over

prolonged import restrictions into China persisted. This saw RBCT prices fall too via the FOB spread.

Energy markets were generally stronger, with carbon prices abating somewhat since hitting recent

highs.

Capesize freight rates have continued to trend higher, keeping delivered coal prices into SE Asia robust, even as power demand wanes amidst weak Asian LNG prices. India’s Power Minister

has re-iterated that non-fossil fuel sources (nuclear, hydro and renewables) will account for 60% of

generation capacity by 2030, up from around 37% currently.

Meanwhile, Indian coal demand is expected to increase slightly going into 2021 as the economy recovers and overall power demand increases.

Chinese President Xi Jinping surprised the world by recently pledging China would aim for “carbon neutrality” by 2060, but Beijing remains concerned about energy security and economic growth, and continues to invest in new coal-fired generation, especially in more remote provinces.

During the JHB Mining Indaba, Sir Mick Davis said that, “Eskom can be relatively easily fixed in

three or so years, but it needs a cash injection from the state, the urgent reintroduction of skills, sensible coal contracts and to be free of political meddling”. Easier said than done!

Medium term trend (red signal line) is about to break into positive territory, signalling we should see some nice moves to the upside now. Certainly, if the coal price is to rally, around now would be the right time.

If price remains lacklustre at this point, we could see momentum start to top out, and then one would be tempted to start looking for the bears, and potential bullish capitalution.

For now however, the bulls are (only just) still in the driving seat.

Article Enquiry

Email Article

Save Article

Feedback

To advertise email advertising@creamermedia.co.za or click here

Research Reports

Projects

Latest Multimedia

Latest News

Showroom

Multotec, recognised industry leaders in metallurgy and process engineering help mining houses across the world process minerals more efficiently,...

VISIT SHOWROOM

Iritron delivers advanced automation, control, and optimisation solutions to the Mining, Minerals & Metals, Consumer Package Goods and...

VISIT SHOWROOM

Announcements

What's On

Subscribe to improve your user experience...

Option 1 (equivalent of R125 a month):

Receive a weekly copy of Creamer Media's Engineering News & Mining Weekly magazine

(print copy for those in South Africa and e-magazine for those outside of South Africa)

Receive daily email newsletters

Access to full search results

Access archive of magazine back copies

Access to Projects in Progress

Access to ONE Research Report of your choice in PDF format

Option 2 (equivalent of R375 a month):

All benefits from Option 1

PLUS

Access to Creamer Media's Research Channel Africa for ALL Research Reports, in PDF format, on various industrial and mining sectors

including Electricity; Water; Energy Transition; Hydrogen; Roads, Rail and Ports; Coal; Gold; Platinum; Battery Metals; etc.

Already a subscriber?

Forgotten your password?

Receive weekly copy of Creamer Media's Engineering News & Mining Weekly magazine (print copy for those in South Africa and e-magazine for those outside of South Africa)

➕

Recieve daily email newsletters

➕

Access to full search results

➕

Access archive of magazine back copies

➕

Access to Projects in Progress

➕

Access to ONE Research Report of your choice in PDF format

RESEARCH CHANNEL AFRICA

R4500 (equivalent of R375 a month)

SUBSCRIBEAll benefits from Option 1

➕

Access to Creamer Media's Research Channel Africa for ALL Research Reports on various industrial and mining sectors, in PDF format, including on:

Electricity

➕

Water

➕

Energy Transition

➕

Hydrogen

➕

Roads, Rail and Ports

➕

Coal

➕

Gold

➕

Platinum

➕

Battery Metals

➕

etc.

Receive all benefits from Option 1 or Option 2 delivered to numerous people at your company

➕

Multiple User names and Passwords for simultaneous log-ins

➕

Intranet integration access to all in your organisation